India Glycols Ltd - annual EPS increased 38%

A chemical company poised to benefit from the ethanol blending initiative

Note - We are observing precaution in the current market conditions. The market sentiment is very high on greed currently, with NIFTY50 making newer highs. But the broader market(NSE:CNX500) is showing opposite signs. Only few large cap stocks are participating in the rally, and majority of the mid and small cap stocks are not holding their breakouts. Both small and mid-cap indexes have been underperforming compared to NIFTY50 in the last 3 weeks. A correction in the overall market is anticipated and protecting capital is important.

Company name - India Glycols Ltd

Last closing price(NSE:INDIAGLYCO) - ₹1354.95 (as on 1-Oct-2024)

Estimated reading time - 3 minutes

We recently covered RPG Life Sciences Ltd on 22-Sep, and the timing of our analysis worked out as it reached +10% yesterday. The updated performance of all our past analyses is available here.

Executive Summary

Established in 1988, India Glycols Ltd. is engaged in the manufacturing of green technology-based bulk, specialty & performance chemicals, and natural gums, spirits, industrial gases, sugar, and nutraceuticals.

The govt. is targeting an Ethanol Blending of 20% by ESY 25-26 and this provides an opportunity for growth for the company.

The company has reported significant sales growth in the last 3 quarters, with 40.58% growth in Q1 - 2025.

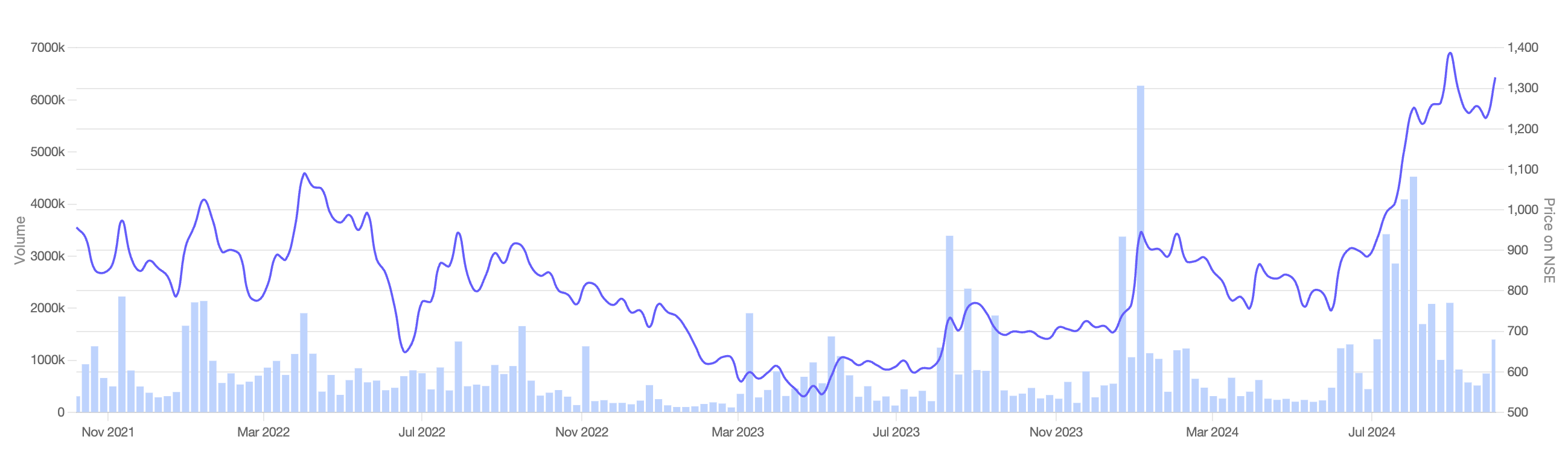

Stock price chart

Detailed analysis

About the company

Established in 1988, India Glycols Ltd. is engaged in the manufacturing of green technology-based bulk, specialty & performance chemicals, and natural gums, spirits, industrial gases, sugar, and nutraceuticals.

The company operates 4 business segments - Bio-Based Specialties and Performance Chemicals (BSPC), Bio-fuel, Potable Spirits (PS) and Ennature Biopharma (EB).

The annual net profit increased by 22% and EPS increased by 38%.

Future prospects

What is the company’s plan to maintain earnings growth in future?

Govt. is targeting an Ethanol Blending of 20% by ESY 25-26 and this provides an opportunity for growth for the company.

New biofuels portfolio helping build top line as well as bottom line.

Potential risks that can hamper the future growth?

Cost Pressures: Despite growth, the company faces ongoing cost pressures, particularly in raw materials and logistics.

Finance Costs: Rising finance costs due to increased term loans and higher interest rates; expected to remain elevated until FY25-26.

Market Dynamics: Uncertainty in margin improvement for the biofuels segment due to fluctuating grain prices and energy costs.

Financial analysis

Overview

The promoter holding is 61%, and pledged percentage is 0%.

The debt-to-equity is 0.66 and the price to book value ratio is 2.03.

Quarterly results

Growth in key metrics in the latest quarter Q1 - 2025 compared to the last year’s same quarter -

The company has reported significant sales growth in the last 3 quarters, with 40.58% growth in Q1 - 2025.

The operating profit increased by 26%.

The net profit increased by 17% and EPS increased by 18%.

Annual results

Growth in key metrics in the last financial year 2024 compared to the previous financial year -

The company reported a sales growth of 24.26%, and operating profit growth of 36%.

The net profit increased by 22% and EPS increased by 38%.

Peer comparison

The company has a the lower P/E among it’s peers at 22.54, while having the highest sales growth at 41.15%.

The 3 peers valued more than India Glycols in the above table have lesser total sales, profits but have much higher current market cap. This shows a potential for India Glycols Ltd stock price to grow, if it is able to maintain it’s sales growth.

Did you find our analysis on India Glycols Ltd valuable? Help us reach more investors like you.

This is not a stock recommendation. It’s an analysis of the stock basis the data available today, and the viewpoint can evolve in future. Please read our Disclaimer here.

Credits : Financial data source - screener.in